ExchangiFi LLC, the platform for Section 351 tax-deferred exchanges, today released a white paper estimating that $5.0 trillion in U.S. taxable equity assets are structurally suited to convert into exchange-traded funds via Section 351 of the IRC.

The paper, “The Structural Distribution of American Taxable Equity Wealth and the Strategic Landscape for Section 351 ETF Conversions,” draws on Federal Reserve Z.1 data, IRS aggregates, and industry research. It finds that American households hold $57.7 trillion in corporate equities and fund shares, with roughly 87% held by the top 10% of households. Much of that wealth carries large embedded gains. For a top-bracket California resident, selling can cost 37.1% of a position once federal, surtax, and state layers are combined.

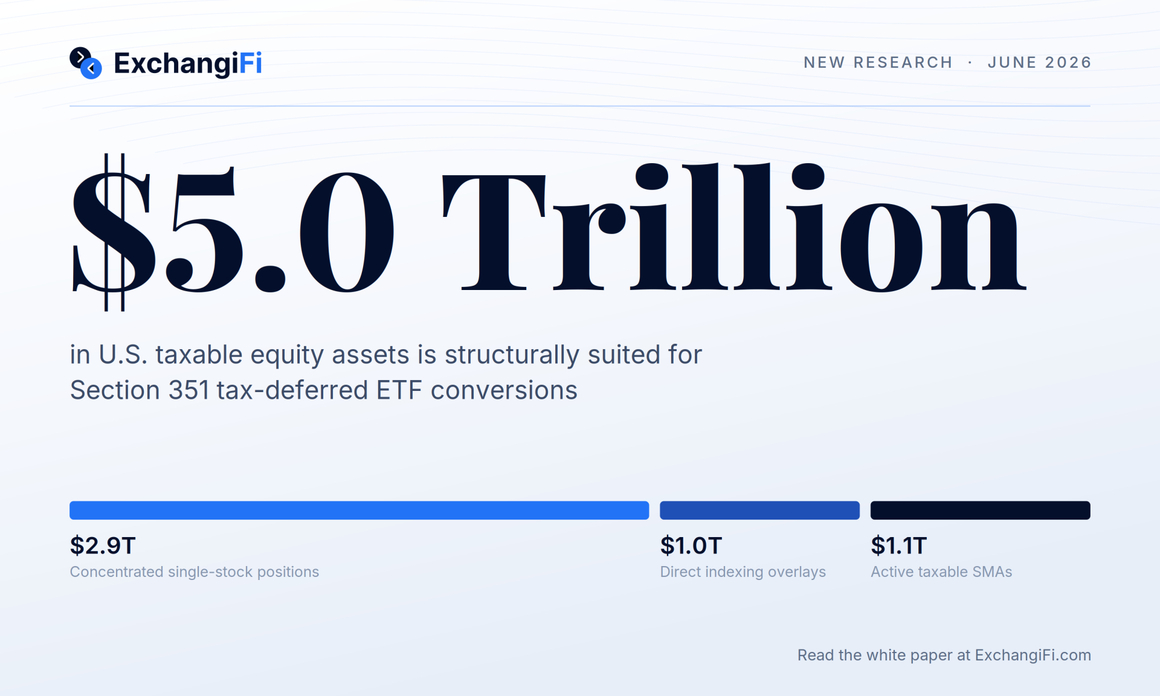

The research presents splits the addressable market into three pools. An estimated $2.9 trillion sits in low-basis concentrated single-stock positions. An estimated $1.0 trillion sits in tax-aware overlays and direct-indexing accounts where loss harvesting has plateaued. An estimated $1.1 trillion sits in actively managed taxable equity SMAs subject to annual turnover tax drag of an estimated 100 to 200 basis points and high fees. The paper excludes roughly $150 billion in leveraged long/short assets, which cannot qualify because short positions are liabilities rather than transferable property.

“Financial advisors have a fiduciary duty to diversify their clients portfolios, and to minimize taxes, which are often in direct conflict,” said Matthew Bucklin, Founder and Chief Executive Officer of ExchangiFi. “I founded ExchangiFi because the demand for these conversions is measured in trillions and the bottleneck is operational. Building compliant baskets, running the diversification tests, and executing the in-kind transfer cleanly is software work, and we built the software.”

The paper also addresses the fiscal question directly. Measured against the strategies wealthy holders actually use, including borrowing against positions and holding until the Section 1014 basis step-up erases the gain at death, the research argues a Section 351 conversion is most likely revenue-neutral. The investor’s cost basis carries into the ETF and the gain remains in the tax base until shares are eventually sold.

The white paper covers the legal guardrails in detail, including the Section 351(e) diversification tests, the 80% control requirement, and the anti-abuse constraints around pre-arranged dispositions, stuffing, and sequential seeding. The full paper is available at ExchangiFi.com.

About ExchangiFi LLC

ExchangiFi operates an independent marketplace platform connecting wealth managers and ETF issuers to facilitate Section 351 tax-deferred exchanges. The platform automates compliance testing, portfolio optimization, and transaction coordination, replacing manual processing with auditable software. ExchangiFi is based in Palm Beach Gardens, Florida. Financial advisors and ETF sponsors can learn more at ExchangiFi.com.

Contact

Founder & President

Matt Bucklin

ExchangiFi

[email protected]

Disclaimer: This content was supplied by the news source, company, or organization identified in this release. Prodigy and its distribution partners have not independently verified the facts, figures, claims, statements, financial information, user metrics, funding announcements, business results, or other representations contained herein.

Publication of this content does not constitute an endorsement, recommendation, approval, verification, or guarantee by Prodigy or any distribution partner. Readers, investors, journalists, customers, and other stakeholders should perform their own independent investigation and due diligence before making any decisions based on the information presented.

All responsibility for the accuracy and validity of the information contained in this release rests solely with the issuing organization and its representatives. Prodigy expressly disclaims any liability for errors, omissions, inaccuracies, or reliance on the information contained in this announcement.